Share on Facebook

Share on Facebook Share on X

Share on X Share by Email

Share by Email Share on Google Classroom

Share on Google Classroom

The two principal types of banks are central banks and commercial banks, or chartered banks as the latter are called in Canada. A central bank such as the Bank of Canada operates as an arm of the federal government, carrying out its monetary policy, acting as a lender of last resort to the chartered banks, holding deposits of governments and chartered banks, and issuing notes or money.

The chartered banks accept deposits from the public and extend loans for commercial, personal and other purposes. Other financial institutions, known as “near-banks,” perform some of these functions, but banks are the only institutions that can increase or contract the basic money supply. In addition to these traditional functions of the banking system, the banks have increasingly moved to provide a wider range of services such as investment banking, international banking services, information processing and real estate operations.

History

In one of the earliest codes of law, compiled by Hammurabi, king of Babylon from 1792 to 1750 BC, several paragraphs were devoted to banking. By about 1000 BC, in Babylon the transfer of bank deposits to a third party was common, and the palace or temple extended loans from its own assets. The Greeks established private banks, which accepted deposits and acted as agents in the settlement of debts. Pasion of Athens, a famous 4th-century BC banker, invested his own funds and those of his depositors in commercial ventures. Roman bankers acted as money changers, auctioneers, discounters and creditors; they formed a banking association and maintained something similar to a modern current accounts system.

The word bank derives from the Italian word banco, the bench on which money changers sat to conduct their business, and from the 5th to the 11th century bankers acted primarily in this capacity. With the advent of the Crusades, the Lombards, northern Italian merchants, formed merchant guilds; they accepted deposits, granted advances and made payments, preferring to operate where they were not required to pay taxes. In the 12th century, the Lombards established themselves in London, and Lombard Street remains a symbol of financial power.

From the 14th to the 19th century, various banks were established in countries such as Italy, Holland, Spain, France, Germany and England. The Bank of Amsterdam was established in 1609 and acted as a guarantor of coinage, since it would accept coins only at what it perceived as their real value. The Bank of Stockholm, founded at about the same time, issued receipts for deposits that were circulated for purchasing goods and as bills of exchange-in effect, the first bank notes (see Money). The Bank of England was established in 1694 as a private bank (remaining so until 1946) under a royal charter to raise money for war. Banking history in England is distinguished by the early development and use of the cheque; on the continent, the limitations of the non-negotiable cheque precluded extensive use of deposit credit until well into the 19th century.

Early Banking in Canada

In the earliest days of French settlement in Canada, barter was generally the method of trade and there was no local currency (see New France). The coins and merchandise customarily sent from France returned there for the purchase of imports. One year, when a shipment did not arrive, Intendant François Bigot issued signed playing cards, redeemable in coins and merchandise (when they arrived), and ordered the colonists to accept them as money (see Playing-Card Money). By 1760, the colony was 80 million livres in debt, much of it in worthless ordinances issued by Bigot. After the Conquest, the British used Mexican, Spanish, Portuguese, French and German coins to pay their troops, which, with trade goods, became the coin of the realm.

.", "title_en": "François Bigot, financial commissary ", "caption_en": "François Bigot, the notorious intendant, in an illustration by George D. Warbarton in \"The Conquest of Canada\" (courtesy Library and Archives Canada/C-3718).", "title_fr": "François Bigot, commissaire ordonnateur "})

In 1792, nine Montréal merchants formed the Canada Banking Company, but because it could not obtain permission to issue bank notes it failed, as did two other similar ventures in 1807 and 1808. During the War of 1812, the governor issued “army bills” that bore interest and could be exchanged for cash, government bills of exchange in London or more army bills. In 1817, the Bank of Montreal (a joint-stock operation owned by 289 subscribers) opened its doors in Canada, but did not get approval of its charter until 1822. Two other banks also received their charters about this time — the Bank of New Brunswick (1820) and the Bank of Upper Canada (1821). The Bank of Upper Canada was controlled by the Family Compact, and the legislature of the time refused charters to any group unless some of its members belonged to the oligarchy.

Another bank, the Bank of the People, was established by the enterprising Francis Hincks, who became prime minister of the Province of Canada and was later Sir John A. Macdonald’s finance minister. He was responsible for ensuring the passage of Canada’s first Bank Act (1871) and was later named president of the Consolidated Bank. (He was also brought to trial on various offences and convicted of fraud, although the conviction was reversed on appeal.)

Many of Canada’s first bankers — e.g., Samuel Zimmerman, who was involved in the Great Southern Railway swindle — were not examples of probity, and until the 1920s banks in Canada were generally unstable. Between 1867 and 1914, the failure rate of Canadian banks was 36 per cent as opposed to 22.5 per cent in the United States, costing Canadian shareholders 31.2 times more than was lost to American shareholders. Of the 26 failures in this period, 19 resulted in criminal charges against bank officers or employees. Improved bank regulation reversed these failure rates and Canada has had only two bank failures since 1923, while the US has had over 17,000.

Unlimited Branch Model

The structural organization of the Canadian banks followed the English model of allowing unlimited branches — a model unsuited to promoting industrial development in the colony. Regional growth suffered as well. For example, by 1912, in one area of the Maritimes, only five cents of every dollar deposited in the bank were loaned locally, and 95 cents were transferred to central Canada.

In addition, the number of banks in Canada was restricted by high capital requirements and vested interests allied to the legislators. Attempts by Westerners to form their own bank were vetoed by the Canadian Bankers’ Association, officially incorporated in 1901. As a result, the Canadian banking system became characterized by the creation of a few dominant banks with many branches, compared to the American practice of encouraging many unit banks and restricting or prohibiting branches.

Bank charters were issued by Upper Canada and Lower Canada until 1867 and subsequently by the federal government. Thirty-eight banks were chartered by 1886 and this number changed little until the First World War, when it declined sharply, and only eight remained, of which five were nationally significant. Legislative changes and the economic expansion of the West reversed this trend. As of 2014 there were 32 domestic banks operating in Canada, as well as 23 foreign bank subsidiaries, 28 full-service foreign bank branches, and four foreign bank lending branches, according to the Office of the Superintendent of Financial Institutions.

Banking practices and financial institutions changed and evolved as the economy developed in the 19th century. At this time, the banks issued their own notes, which were used as money, but gradually governments supplanted this privilege until finally only the Bank of Canada could issue legal tender. Lending practices evolved from the primary banking function of making commercial loans that were self-liquidating within a year to making loans on grain secured by warehouse receipts, on proven reserves of oil in the ground and in the form of mortgages on real estate.

Other financial institutions providing some of these banking functions also began appearing early in Canadian history. Mortgage loan companies patterned after building societies in Britain opened in the 1840s and they evolved into “permanent” companies (e.g., the Canada Permanent Mortgage Company, selling debentures and investing in mortgages). Trust companies were also formed during this time to act as trustees and professionally manage estates and trusts; they gradually assumed banking functions (e.g., providing savings and chequing accounts) and became major participants in the mortgage market. Most of these financial institutions have been absorbed into the banking system in recent years, through mergers and acquisitions as a result of legislative changes, financial problems created by heavy loan losses, and because of a lack of economies of scale.

The other major type of near-bank is the savings and credit co-operative, called a credit union in most of Canada and a caisse populaire in some areas. After a slow start in the first half of the 20th century, credit unions grew rapidly by using deposits to extend loans to their members.

Role of Banks in Canada

As is true with all financial institutions, the basic function of banks is to channel funds from individuals, organizations and governments with surplus funds to those wishing to use those funds, which is why they are called financial intermediaries. But banks also have a premier position in this intermediation because of their role in providing the payment system, while acting as the vehicle for Canadian monetary policy and as the federal government’s instrument for some social and political policies. Consequently, the actions of the banks have a major impact on the efficiency with which the country’s resources are allocated.

In addition to these wider roles, banks also have an obligation to their shareholders to earn an adequate return on their equity and pay sufficient dividends. If these goals are neglected, investors will withdraw their capital from the banking system and force either a contraction of the money supply, or government ownership.

The experience of the early 1980s reveals the conflict that can arise among these purposes and goals in the banking system. The federal government encouraged the banks to extend huge loans to Canadian companies that wished to take over subsidiaries of foreign companies, especially in the oil and gas industry. This was sometimes in defiance of sound banking practice, and it had wider economic implications, such as the misallocation of credit resources, pressure on the Canadian dollar and an inflationary expansion of the money supply. As a result, the domestic loan portfolio of the banks began deteriorating sharply in 1982 to what was then its worst condition of the postwar period.

Loans to the highly cyclical real estate industry accounted for about 120 per cent of bank capital; loans to oil and gas companies such as Dome, Sulpetro and Turbo, to forest product companies and to Massey-Ferguson and International Harvester also threatened the financial strength of the banks.

International lending practices of Canadian banks were equally troubling. Brisk demand and wide profit margins encouraged the larger banks to pursue international borrowers vigorously with the result that their foreign assets increased from $21.7 billion in 1973 to $156.7 billion in 1983. Many of these loans were made to governments or government-guaranteed borrowers on the theory that governments do not default on loans.

By the summer of 1983, more than 40 countries had agreed to, or had applied for rescheduling of their debt, or had accumulated substantial arrears in interest payments. Furthermore, banks began extending new credits to foreign lenders to enable them to pay interest on older loans. This sleight of hand was good for the reported earnings of the banks but did little or nothing to resolve the serious problem of international debt.

Predictably, the results of both domestic and international lending policies were huge losses for the banks and intensified economic malaise and costs for Canadians. In an effort to combat the impact on bank earnings, and to make adequate provision for loan losses, the margin or difference between the prime rate and the interest rates on savings accounts was pushed to a very high level (see Interest Rates in Canada). In 1980, the banks’ prime rate was 15.5 per cent and the rate on bank savings deposits was 12.5 per cent, a “spread” of 3 per cent. Two years later, the prime rate was unchanged, while the savings rate had dropped to 11 per cent, a spread of 4.5 per cent. Borrowers were therefore paying a higher than normal price for money, while savers received less than a normal return. In addition to these penalties, the high proportion of bank assets tied up in non-productive loans restricted the banks’ flexibility in accommodating credit-worthy borrowers.

More than a decade later, in the very low interest rate environment of early 1997, the prime rate had dropped to 4.75 per cent and the savings rate to one half of 1 per cent, leaving the spread basically unchanged. However, during the following year interest rates rose and the prime rate was raised to 7.5 per cent, while the rate on savings accounts increased to 7.5 per cent. Using the banks’ measure of interest spreads (interest income minus interest expense as a percentage of average assets), there was a decline in the spread from 2.9 per cent in 1991 to 2.8 per cent in 1997.

Banking Structure

The Canadian banking system is generally highly competitive, with more than 3,000 companies offering a wide variety of services. Some are highly specialized and operate in niche markets such as credit cards or home mortgages, and others, such as the major banks, compete in all markets. There are six large banks holding roughly half the assets of the financial system.

Despite a wide choice in financial intermediaries, the banking system remains basically a banking oligopoly dominated by the “Big Five” (see Business Elites). These banks were once considered big by international standards, and the two largest were among the top 20 in the world in the 1970s as measured in asset size. As of 2016, none was in the top 20, but three were in the top 50, according to an asset-based ranking by S&P Global Market Intelligence. Canadian banks have declined in relative international standing, which has led to pressure to allow mergers of the largest banks to increase their international competitiveness.

Canada’s big five banks had the following 2016 global size rankings, according to S&P Global Market Intelligence: Royal Bank of Canada (31st),Toronto Dominion Bank (33rd), Bank of Nova Scotia (46th), Bank of Montreal (51st), Canadian Imperial Bank of Commerce (68th). The top five banks in the world were based in China and Japan.

Who Owns Canadian Banks?

The term “bank” can only be used in Canada if the organization has been approved by the Minister of Finance (see Department of Finance). For many decades, there were two types of banks incorporated in Canada. A Schedule I bank had wide public ownership; only 10 per cent of its shares could be owned by a single foreign or domestic investor and only 25 per cent could be owned by all foreign investors (see Foreign Investment). A Schedule II bank was a more closely held Canadian bank or the subsidiary of a foreign bank. Its activities were more restricted.

In 2001, to encourage competition in the domestic banking industry, the federal government changed ownership rules. Three bank categories were created: “large” banks with more than $5 billion in assets, “medium” banks with $1–5 billion in assets, and “small” banks with fewer than $1 billion in assets. Large banks were still required to be widely held, although individual investors were permitted to own up to 20 per cent of voting shares and up to 30 per cent of non-voting shares. Medium banks were allowed to be closely held, but they had to have a public float of at least 35 per cent of their voting shares. Small banks had no ownership restrictions.

Source of Assets and Liabilities

When a bank or other financial institution is incorporated, it begins operations by selling shares to investors, and the funds raised in this manner become the shareholders’ equity. The bank will then try to attract deposits from the public in the form of demand deposits, which can be withdrawn by cheque at any time and which normally pay no interest; savings accounts, which pay a variable rate of interest and have restrictions on their withdrawal; and deposits with a fixed term of a few days to five years, paying a fixed rate of interest. In 2015, the banks had $1.810 trillion in total deposits — chequable, non-chequable and fixed term — held by the general public. All this money is a liability or debt of the banks.

To meet public demand, the banks keep some of their assets in the form of cash and investments, e.g., treasury bills, which can be quickly converted into cash. Most of the remaining financial resources are invested in securities such as bonds and term-preferred shares and in loans and mortgages. In 2015, the banks held total Canadian dollar assets of $2.894 trillion.

Banks, trust companies and credit unions historically concentrated their assets and liabilities in different areas, but this has changed as they competed more in the same markets. The banks monopolized the market for demand accounts at one time because they were the only deposit institution offering bank accounts with chequing privileges; they still control the huge corporate accounts, but the credit unions have been taking a slightly larger slice of the market for personal chequing accounts.

Revenue and Profits

The principal source of revenue for a bank is the interest earned on investments and loans, but they have increasingly added other sources such as service charges, fees and ancillary revenue-generating operations such as investment management and banking, mutual funds, stock brokerage and trust services (see Stock and Bond Markets). Innovations in lending and security markets have also led to a much wider range of services and products and to greater market risks, which in turn have led to sophisticated methods of managing risk through derivative securities and simulation-based risk evaluation models.

The profits of the banks are affected by their ability to develop new revenue sources, the direction of interest rates, the trend in non-performing loans and their success in controlling costs. The most important measures of profitability are the return on average assets and the return on shareholders’ equity.

Banking Operations

Canadian commercial banks, like other investor-owned organizations, are managed by a board of directors, headed by a chairman, which oversees a president and vice-presidents representing special areas of the bank. These boards of banks are considered the most prestigious appointments of all boards; they are large (35 to 50 members) and their members are generally also members of boards of other major companies who may be customers of the bank. These interlocking directorships and the number of directorships held by many of the members would seem to make it difficult for them to fulfil their responsibilities to the bank.

Regulation of Banking

According to the Constitution Act, 1867, banking is regulated by the federal government and property and civil rights are provincial responsibilities. The first Bank Act, virtually drafted by the Bank of Montreal, put Maritime banks under the control of federal banks. In 1891, the Bankers Association (later the Canadian Bankers Association) was founded. A powerful lobby group, it was given the right to determine whether bankers received charters. Under the regimes of both Sir John A. Macdonald and Sir Wilfrid Laurier, bankers effectively chose the ministers of finance by threatening to excite financial crises if the candidates suggested by the prime ministers were approved.

")

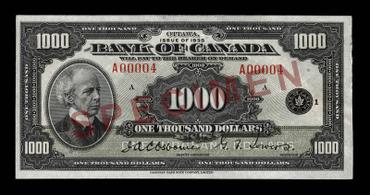

\", \"source_en\": \"(courtesy Bank of Canada)\", \"caption_fr\": \"Voici la seule coupure de 500 dollars jamais émise par la Banque du Canada. Elle montre sir John A. Macdonald, le premier \u00e0 occuper la fonction de premier ministre du Canada, portant un manteau \u00e0 col de fourrure.\", \"title_en\": \"Front of the $500 Note (1935\u201337)\", \"caption_en\": \"This was the only $500 note ever issued by the Bank of Canada. It features a portrait of Sir John A. Macdonald, Canada")

In 1964, the Royal Commission on Banking and Finance (the Porter Commission) recommended “a more open and competitive banking system.” Its suggestions led to major reforms and changes. The 1967 Bank Act revision lifted the 6 per cent annual interest-rate ceiling banks could charge on personal loans and allowed banks to enter the mortgage field. It also barred the previously legal practice of collective rate setting by banks and required banks to inform borrowers better about the real cost of loans (see Interest Rates in Canada).

In the same year, the federal government also passed an act to establish the Canada Deposit Insurance Corporation to provide $20,000 insurance for deposits in banks and federally chartered near-banks. Provincial near-banks were included in most provinces by relevant provincial legislation. The maximum insurance coverage was raised to $60,000 in 1983, and then to $100,000 in 2005.

As a result of changes in the Bank Act of 1980, the Canadian Payments Association (now Payments Canada) was established as the agency responsible for the cheque-clearing system; reserve requirements were reduced, which increased bank assets substantially; the minister of finance became the sole arbiter deciding which new banks could be established; foreign banks were allowed to establish themselves and required to keep reserves, but their growth was restricted in various ways; banks were allowed to become involved in the business of leasing large equipment; banks were allowed to become involved in factoring; and banks (but not their subsidiaries) were limited to a 10 per cent holding of residential mortgages.

Subsequent revisions removed restrictions on mortgage lending, allowed the banks to buy and operate trust companies, securities dealers and insurance companies. However, they are still forbidden from providing financing for auto leasing and from selling insurance in their branches. The 1991 revision defined the business of banking for the first time. New regulations have led to a much higher standard of disclosure to consumers regarding the various costs, rights and penalties involved in banking services.

The banks are also regulated by the Bank of Canada under the authority of the Bank of Canada Act through its management of the government’s monetary policy. The Canada Deposit Insurance Corporation and the Office of the Superintendent of Financial Institutions carefully monitor the banks for financial soundness and compliance.

Future of Banking

Technological advances in banking have led to major improvements in banking services. Electronic Funds Transfer, in which funds are transferred through electronic messages instead of by cash or cheque, enabled the banks to introduce multi-branch banking, automatic bank machines (ABMs), more credit card services, debit cards, home banking, electronic data interchange, automated payments of regularly recurring expenses and direct deposits of government, payroll and other cheques. On the horizon are ABMs that allow users to buy or sell mutual funds, make loan applications and even possibly provide other services currently available in some European countries such as buying bus tickets and postage stamps or exchanging foreign currency (see Exchange Rates).

The enormous data banks created by these new systems have enabled the banks to assign costs more accurately to individual banking transactions and thereby charge fees for these services that reflect these costs. They have also raised privacy concerns because of the large amount of personal information accumulated about bank customers.

Massive Reforms

In 2001, massive bank reform legislation had the clear aim of making Canadian banking more consumer-friendly. The reforms created the Financial Consumer Agency of Canada to enforce consumer-related provisions of the legislation, monitor the industry’s self-regulatory consumer initiatives, promote consumer awareness and answer consumer questions (see also Consumer Standards).

In addition, banks were required to open accounts for individuals without demanding a minimum deposit or that the individual be employed. They were required to make low-cost accounts available to consumers with a maximum monthly fee. And financial institutions were required to cash government cheques for non-customers with a minimum form of identification.

Also added was a requirement that federal deposit-taking institutions give four months’ notice of a branch closure and post the notice in the branch. In areas where there is no other financial institution within 10 kilometres, advance notice of six months was required to give rural communities time to come up with alternatives.

The legislation also gave the federal government more authority to regulate in areas such as disclosure of bank policies on hold periods for deposits. It also expanded an existing prohibition on tied selling. This was in response to consumer complaints of being forced to do business with a bank as a condition of getting a loan. The Act forbade any condition forcing a customer to buy any financial services product in order to get any other product, not just a loan.

The new legislation also required banks to be members of a third-party dispute resolution service to iron out customer disputes. But that provision was largely a formality of an existing situation. In 1996, the banking industry had voluntarily set up an independent ombudsman’s office to resolve customer complaints about banks and investment dealers. The Ombudsman for Banking Services and Investments (OBSI) operates with a board of directors and staff independent from the banking industry.

In 2008, some of the supporting banks began to express dissatisfaction with the OBSI and subsequently withdrew their support. As a result, the Royal Bank of Canada and Toronto-Dominion Bank contracted an independent arbitration firm to iron out customer disputes their staff was unable to resolve. The move prompted criticism that the two banks were undermining the ombudsman’s authority. But the federal government did not object. In 2010, the government formally required all banks to take unresolved disputes to an independent third party that is approved by the government. The Canadian Bankers Association now lists two industry ombudsmen to resolve customer disputes: the OBSI, which is still supported by most banks, and A.R. chambers for RBC and TD customers.

Canadian Banks Survive the Great Recession

The financial collapse of Wall Street and other financial credit markets in 2008 sent governments around the world scrambling to shore up their banking systems. But Canada’s system was relatively unaffected. The World Economic Forum said that Canada had the strongest banking system in the world in October 2008. That strength is one reason why Mark Carney, then Governor of the Bank of Canada, became the world’s top banking regulator as head of the Swiss-based Financial Stability Board (FSB) in November 2011. No Canadian banks were on the FSB’s critical “too big to fail” watch list of banks whose failure could put the world economy in danger.

Like most banks around the world in 2008, the Canadian banking industry relied heavily on wholesale sources for more than half its funding. But Canadians had what was regarded as a strong retail base to account for 30 per cent of funding. They also relied less on securitisation and repos at 20 per cent of their deposit base.

Canadian banks were able to take advantage of liquidity facilities provided by the Bank of Canada in order to remain immune to the global banking crisis. They were also able to raise medium-term capital by selling insured residential mortgages under the Insured Mortgage Purchase Program, offered by the Canada Mortgage and Housing Corporation, a crown corporation offering mortgage insurance.

(See also Recession of 2008–09 in Canada.)

Mortgages and Holding Companies

Because the global economic crisis had its origins with the collapse of the US housing bubble, Canadian regulators have continued to keep a close eye on a very brisk Canadian real estate market. In October 2008, Finance Minister Jim Flaherty banned 40-year residential mortgages just a year after first allowing them, although Canadian banks had already started withdrawing them six months earlier. In July 2012, Flaherty capped Canadian residential mortgages at 25-year amortizations, eliminating 30-year mortgage loans.

The 2001 reforms also somewhat loosened the ownership restrictions on banks. And they allowed banks and insurance companies to create regulated non-operating holding companies. The introduction of holding companies did not expand the powers of banks or insurance companies. However, their creation allowed flexibility in corporate structures. For example, with the 2001 reforms it became possible for a bank holding company to have a banking subsidiary, insurance subsidiary, securities subsidiary and a subsidiary for unregulated activities. As a result, the four distinct pillars of the financial system envisioned by the Porter Commission of 1964 — banking, insurance, trust companies and securities — became blurred into one financial services sector.